Semiconductors on the AI Wave: What's Behind the Sector's Record 2026

An Nvidia processor. Credit: Nvidia

Since the start of 2026, semiconductor ETFs have become some of the market's leaders: SMH is up about +71%, and SOXX nearly +96% (as of June 16). But behind those impressive returns lies a much longer story. Over the past five years, the sector has gone through a rapid rise and a correction of more than 30% before climbing back to the top. Let's look at why semiconductors became the backbone of the AI economy, what's fueling the industry's growth today, and what risks hide behind such a powerful rally.

Five Years: From Boom to Bust and Back to Growth

To understand why the sector ended up among the market leaders, it helps to look at the past five years: each stage reshaped how investors saw the semiconductor industry.

2021 – shortage. The pandemic sharply changed the structure of demand for electronics. People bought laptops, monitors, game consoles, and other gear for remote work and home en masse. At the same time, automakers ran into a chip shortage: modern cars already depended on dozens, even hundreds, of electronic components. Production capacity couldn't keep up with demand, lead times stretched out, and the chip shortage became one of the main topics in the global economy. Against this backdrop, semiconductor companies rose along with expectations that demand would stay high for a long time.

2022 – crash. Then the market turned sharply. The Fed began raising rates aggressively, and tech stocks – especially high-multiple names – came under pressure. At the same time, pandemic demand started to fade: PC and smartphone sales fell, manufacturers' and distributors' inventories overflowed, and prices for memory and some components dropped. Investors quickly reset their expectations for the sector. Over the year SMH lost about −33%, SOXX about −35%. Semiconductors reminded the market that this is not only a growth story but also a cyclical industry, sensitive to rates, inventories, and end demand.

2023 – turning point. A new phase was opened by the generative-AI boom. After the launch of ChatGPT, the market's focus shifted from consumer electronics to computing infrastructure for data centers. The scarcest resource became not ordinary chips but GPUs and accelerators for training and running AI models. Nvidia became the symbol of this wave, and the whole sector started to be repriced on a different logic: no longer as a set of cyclical component makers, but as the backbone of a new technology infrastructure. Over the year SMH gained more than +73%, and the market effectively began pricing in long-term demand from AI.

2024–2025 – the trend takes hold. Growth continued, but became more selective. Investors started looking not just at the sector as a whole, but at which companies actually benefit from AI capex. Hence the divergence between the ETFs: in 2024 SOXX lagged SMH noticeably because of their different holdings and different weightings of Nvidia and other AI-infrastructure leaders. The main driver was the capital spending of the largest tech companies on data centers, servers, GPUs, networking equipment, and power capacity. Semiconductors finally turned from "hardware suppliers" into a key link in the AI economy.

2026 – the surge. In 2026, the market's bet on AI infrastructure grew even stronger. Spending by the largest tech companies keeps rising, demand for computing power stays high, and investors see semiconductors as a direct way to take part in the rise of AI. As a result, the sector is posting record growth and once again ranks among the market leaders. In essence, over five years semiconductors have run a full cycle: from the pandemic shortage and demand frenzy, through a sharp cyclical downturn, to a new phase of structural growth, where chips have become the foundation of data centers, AI models, and the entire digital infrastructure.

Annual returns of the SMH and SOXX ETFs, 2021–2026. Source: Yahoo Finance, as of June 16, 2026.

What's Driving the Sector Now

The main growth engine is the race for AI infrastructure. The largest tech companies are building data centers, buying up GPUs, expanding cloud capacity, and effectively creating a new industrial layer for the artificial-intelligence economy.

The scale of this investment is already comparable to entire industries. By some estimates, in 2026 Amazon, Alphabet, Meta, Microsoft, and Oracle could direct around $700 billion toward infrastructure, with roughly three-quarters of that spending tied to AI. That's almost two-thirds more than a year earlier. Individually, the picture looks like this: Amazon – about $200 billion, Alphabet – $175–185 billion, Meta – $115–135 billion, Microsoft – more than $120 billion, Oracle – about $50 billion.

A large share of this money ultimately flows through the semiconductor chain: GPUs, networking chips, memory, server components, data-center equipment, and manufacturing capacity. The main beneficiary is Nvidia. Its data-center business is growing explosively: quarterly revenue for the segment reached $75.2 billion, with year-over-year growth of 85–92%. The company's share of the AI-accelerator market is estimated at around 81%, which is why Nvidia remains the main driver of the whole sector's re-rating.

But the story is already bigger than one company. Rising demand is spreading to memory makers, equipment suppliers, contract foundries, networking developers, and the entire infrastructure around AI data centers. So the semiconductor market is growing not just on hype around individual stocks, but on a real expansion of capital spending.

The industry association SIA expects the global semiconductor market to grow 26% in 2026 and top $1 trillion for the first time. Bank of America is even more aggressive: around $1.3 trillion as soon as 2026, and up to $2 trillion by 2030. If these estimates play out, semiconductors will firmly establish themselves as one of the key infrastructure industries of the AI economy.

Semiconductor manufacturing. Illustration: iStockphoto

SMH and SOXX: What's the Difference

SMH and SOXX both give exposure to the semiconductor sector, but they do it differently. That's why their returns can diverge noticeably even over the same market period.

VanEck's SMH is more concentrated in the sector's largest companies, primarily Nvidia. When the market rises on the back of a few AI-infrastructure leaders, that structure works in its favor: the fund reacts faster to gains in Nvidia, TSMC, Broadcom, and other major players. That's why in 2024 SMH clearly outpaced SOXX: +39.1% versus +12.9%.

iShares' SOXX is built in a more diversified way and distributes its weights differently. When the rally broadens and more companies across the semiconductor chain join the move, that structure can have an edge. You can see it in 2026: SOXX is up almost +96%, while SMH gained about +71%.

Both funds hold the key players of the AI chain: Nvidia, TSMC, Broadcom, AMD, ASML, Qualcomm, and Micron. But the role of these companies in the portfolios differs. Nvidia and TSMC offer a direct bet on computing and the manufacturing of advanced chips, ASML – on the lithography equipment without which modern process nodes are impossible, Micron – on memory, Broadcom and AMD – on accelerators, networking, and server infrastructure.

So the difference between SMH and SOXX isn't that one fund is "better" than the other – it's in the structure of the exposure. SMH leans more on the sector's largest leaders, while SOXX is a broader bet on the semiconductor chain.

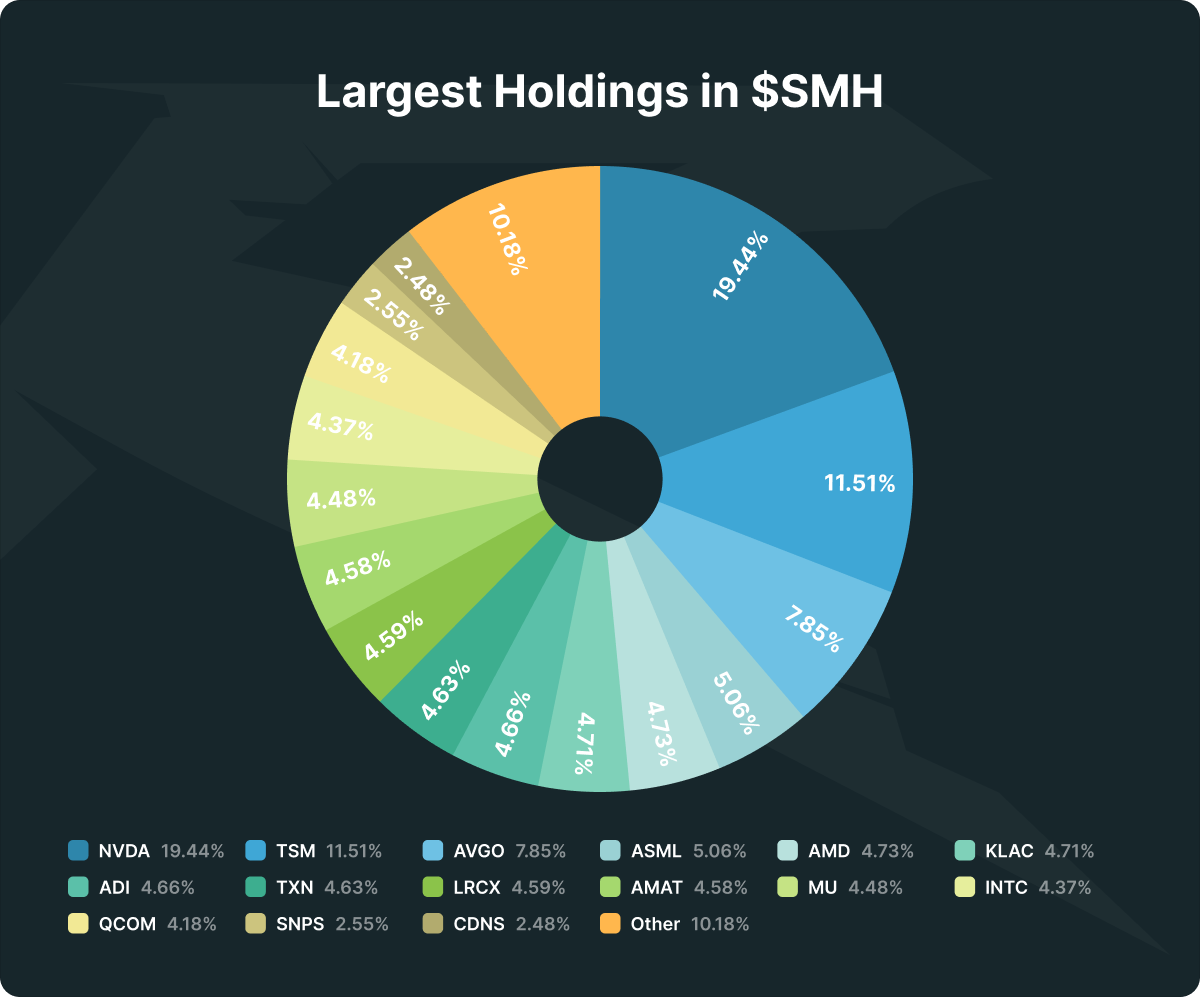

The largest holdings in the SMH ETF: Nvidia (19.4%), TSMC (11.5%), Broadcom (7.9%) and others.

The Flip Side: Risks

High returns come with high volatility. 2022 showed the sector can fall by a third, and its cyclicality hasn't gone anywhere. A large part of the future growth is already priced in, and the heavy concentration in a few names – Nvidia, TSMC, Broadcom, AMD, ASML – makes the funds sensitive to news from these companies and to capex forecasts. If the giants slow their data-center spending, the semiconductor sector will be the first to feel it.

How to Access This with Regolith

On the Regolith marketplace, the semiconductor sector is available through the SMH and SOXX ETFs, with an entry threshold from $50. For an investor, it's a way to get exposure to a whole basket of key AI-infrastructure companies at once – from GPU and memory makers to suppliers of lithography equipment and contract foundries.

This format reduces dependence on any single stock and lets you take part in the sector's growth through a diversified instrument.

This material is for informational purposes only and does not constitute investment advice. Past performance does not guarantee future results. Return figures are as of June 16, 2026.