The venture capital market has grown to $3.5 trillion: why investors struggle to get their money back

Venture capital has evolved from a niche source of startup funding into a vast industry with nearly $3.5 trillion in assets under management. More than 250,000 companies have received funding over the past 20 years. Yet as the market has expanded, a new problem has emerged: capital is remaining locked in private companies for much longer than investors originally expected.

That is the central conclusion of The Future of Venture Capital: Unlocking Liquidity and Growth, a report published by the World Economic Forum and Stanford Graduate School of Business. According to its authors, the venture industry must do more than attract capital. It also needs to restore the mechanisms that return money to investors, allowing them to sell positions, receive distributions and reinvest in new funds and companies.

How the venture capital cycle works

A venture fund raises capital from institutional and private investors, builds a portfolio of stakes in private companies and expects those holdings to appreciate over several years. However, when a startup completes a new financing round at a higher valuation, the value of the fund’s stake rises only on paper. Actual returns are generated only when the investment is sold.

The main exit routes are:

- an IPO followed by the sale of shares on the public market;

- the sale of the company to a strategic buyer;

- the sale of the stake to another investor on the secondary market.

Once an exit takes place, the fund realizes its return, distributes capital and profits to its investors and closes part of the investment cycle. Those proceeds can then be committed to new funds, which in turn finance the next generation of private companies.

This cycle is now slowing down. Private funding volumes and company valuations continue to rise, but the number of IPOs and major M&A transactions remains insufficient. As a result, unrealized value is accumulating across venture portfolios and the time required to return capital is increasing.

For investors, this means lower liquidity and a longer investment horizon. For funds, it means fewer distributions and greater difficulty raising new strategies. Until older investments are converted into cash, capital returns to the market more slowly and is less efficiently redeployed into new companies.

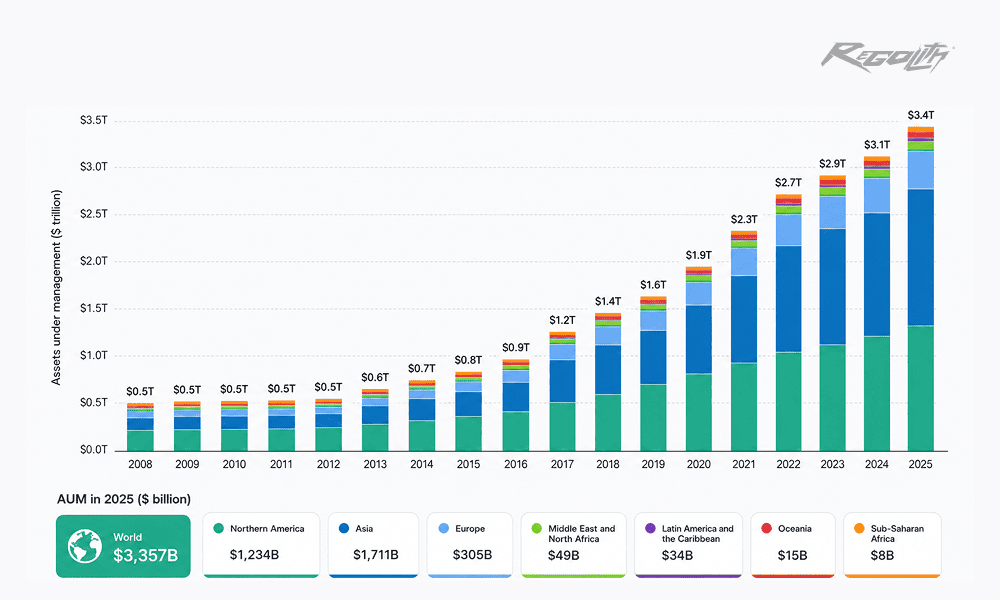

Global venture capital assets under management by region, 2008–2025. Source: Stanford GSB Venture Capital Initiative calculations based on PitchBook data.

$3.2 trillion in unrealized value

According to the report, venture fund portfolios now contain approximately $3.2 trillion in unrealized value. This represents the estimated value of stakes that funds have not yet sold. It appears in portfolio reporting, but it is not cash that investors can access.

Suppose a fund invested $10 million in a startup and the company later raised a new round at five times the previous valuation. On paper, the fund’s stake may also be worth roughly five times more. But until someone buys that stake, the fund has not realized a cash profit.

If market conditions weaken, the company may complete its next round at a lower valuation or face limited demand for its shares. A high reported portfolio value therefore does not guarantee a comparable return when the investment is eventually sold.

This matters particularly for venture funds because their investors often include pension funds, insurance companies, universities, family offices and sovereign wealth funds. These institutions need cash distributions to meet their own obligations and allocate capital to new funds.

Startups are staying private for longer

One of the main causes of the growing liquidity gap is the longer period between a company’s first venture round and its eventual IPO.

As of March 31, 2026, there were 1,920 private companies worldwide valued at $1 billion or more. Of these, 59% had been founded more than ten years earlier, while one in five was more than 15 years old.

Remaining private for longer can benefit a startup. The company avoids quarterly reporting requirements, retains greater management flexibility and can raise large amounts of capital from private investors without the pressure of public markets.

For early investors and employees, however, this means a longer wait. Their shares may be worth millions of dollars on paper, but that wealth cannot be used to buy a home, diversify a portfolio or make new investments without a transaction.

In the past, a successful venture-backed company would typically move toward an IPO after reaching a certain scale. Today, the largest startups can raise private rounds worth tens of billions of dollars and postpone a listing. The private market is therefore taking on functions once performed by public exchanges, without offering comparable liquidity or transparency.

Why the venture market lacks liquidity

The problem extends beyond individual investors having to wait longer.

When a venture fund does not sell mature assets, it cannot distribute capital to its investors. Those investors then become more cautious about committing money to new funds. This reduces the amount of capital available to emerging managers and early-stage companies.

The result is a self-reinforcing cycle:

fewer IPOs and company sales → fewer returns to investors → fewer commitments to new funds → less capital for new startups.

This dynamic is particularly difficult for smaller funds. Large managers can raise capital based on their brand, track record and long-standing relationships with institutional investors. Newer teams without an established history face a much harder fundraising environment.

The market therefore becomes concentrated at two levels. Capital flows toward the largest venture firms, which then allocate an increasing share of their money to a limited number of high-profile companies.

The secondary market is accelerating capital returns

As the IPO market has remained weak, trading in private company shares has expanded rapidly. On the secondary market, an investor, founder or employee sells existing shares to another buyer. The company itself usually does not receive new capital, but the seller gains liquidity without waiting for an IPO or a full acquisition.

In 2025, secondary transactions involving US venture assets were estimated at $106.3 billion. Approximately $91.7 billion came from direct transactions in company shares, while $14.6 billion came from fund-led deals. In scale, the secondary market has moved closer to traditional exit channels such as IPOs and acquisitions.

These transactions can take several forms:

- Direct share sale. An employee or early investor sells a stake to a new buyer.

- Tender offer. The company organizes the transaction and determines who may sell, how much they may sell and at what price.

- Sale of a fund interest. An investor sells its position in a venture fund to another institutional buyer.

- Continuation fund. A manager transfers mature assets from an older fund into a new vehicle, allowing some investors to exit while others retain exposure.

The secondary market is gradually losing its reputation as a venue used mainly for distressed or forced sales. It is becoming a standard tool for liquidity planning, employee compensation and portfolio management.

Liquidity remains concentrated among market leaders

Despite its rapid growth, the secondary market does not yet solve the problem for the entire industry. In the fourth quarter of 2025, the 20 most actively traded startups accounted for 86.4% of transaction value on the Hiive platform. The five largest companies represented 55.6%.

This means secondary-market liquidity is primarily available for well-known private companies with high valuations and sustained investor demand. Before its IPO, shares in SpaceX were significantly easier to buy or sell than shares in a less established startup. Today, a similar pattern persists around OpenAI, Anthropic, Stripe, Databricks and Revolut. The secondary market therefore reduces the pressure, but does not eliminate it.

For liquidity to expand across a broader range of companies, the market needs:

- more transparent pricing;

- standardized transaction rules;

- better access to reliable financial information;

- simpler legal infrastructure;

- a larger pool of buyers;

- more trading beyond a small group of leading companies.

Without these improvements, the secondary market risks reproducing the same concentration already visible in primary venture funding.

AI is intensifying capital concentration

Artificial intelligence has become the largest source of new venture investment, but it has also made the market even more concentrated. In the first quarter of 2026, global venture funding reached approximately $297 billion. OpenAI, Anthropic, xAI and Waymo together raised about $188 billion, representing roughly 63–65% of all global venture funding during the quarter.

The reason is clear. Developing frontier AI models requires enormous spending on chips, data centers, electricity, research teams and cloud infrastructure. As a result, industry leaders are raising rounds that would once have been unusual even for mature public companies.

For investors, this concentration creates both opportunity and risk. On one hand, a small number of AI companies may become core infrastructure for the global economy and generate exceptional returns. On the other, when such a large share of capital is directed toward a handful of companies, funding becomes harder to obtain for the rest of the startup market. High valuations also raise expectations for future revenue, profitability and growth.

A large funding round does not create liquidity by itself. In fact, if a company can continue raising sufficient private capital, it may delay its IPO even longer. The AI investment boom can therefore increase the value of the venture market while simultaneously worsening its core liquidity problem.

Can a new IPO wave unlock capital?

Listings by the largest private companies could partially restart the venture cycle. An IPO converts a private valuation into a public market price and eventually allows early shareholders to sell their positions after the lock-up period expires. For a venture fund, this creates an opportunity to realize returns, distribute proceeds and begin a new investment cycle.

SpaceX’s recent Nasdaq listing demonstrated how years of waiting can ultimately lead to a public-market exit. For the private market, the importance of such an IPO extends beyond its size. A successful listing establishes a valuation benchmark for other companies and increases investor confidence in subsequent offerings.

Regolith’s portfolio also includes companies at different stages of the path toward public markets. Kraken and Discord have previously submitted confidential IPO filings, Dataminr has been strengthening its preparations for a possible listing and Abra has announced plans to list on Nasdaq through a SPAC combination.

However, even several major IPOs will not solve the problem automatically. Public markets must be able to absorb a substantial volume of new shares, while issuers must demonstrate financial performance that supports their private valuations. If newly listed shares perform well, the IPO window may open for the next group of issuers. If prices decline sharply, boards at other private companies may once again postpone their listings.

From secondary transactions to IPOs

At first glance, secondary transactions may appear to compete with IPOs. In practice, the two serve different purposes.

The secondary market provides partial liquidity before a listing. It allows early investors and employees to sell part of their holdings, while giving new investors an opportunity to enter a company before it becomes public.

An IPO creates a broader and more transparent market, where pricing is determined by thousands of participants. It also allows a company to raise new capital and use publicly traded shares for acquisitions and employee compensation.

The prospect of an IPO can even increase activity on the secondary market. Investors are more willing to buy private shares when they see a possible exit within a realistic timeframe. Public listings also establish pricing benchmarks for comparable private companies.

A sustainable venture ecosystem therefore needs both channels: a developed secondary market for interim liquidity and a functioning IPO market for full exits.

What solutions does the report propose?

The World Economic Forum and Stanford identify five areas that could strengthen the venture ecosystem. These include developing secondary-market infrastructure, expanding access to institutional capital, improving conditions for company scaling and creating more efficient mechanisms for returning capital to investors.

The central message is that increasing the amount of money entering the market is no longer enough. The entire financial chain must function more efficiently, from a startup’s first financing round to the sale of a stake and the reinvestment of proceeds.

This will require action from multiple participants:

- Companies should establish clear secondary transaction policies in advance and avoid treating an IPO only as a last resort.

- Venture funds should focus more closely on liquidity management rather than only on rising paper valuations.

- Exchanges and financial platforms can develop private-share trading infrastructure and standardize transactions.

- Regulators can improve access to private markets while maintaining disclosure and investor protection requirements.

- Institutional investors should evaluate managers not only by asset appreciation, but also by their ability to return capital.

What this means for private investors

The growth of the secondary market expands access to well-known private companies, but it does not make these investments equivalent to buying publicly traded shares.

Investors still need to consider several factors:

- Limited disclosure. Private companies provide less financial information.

- Complex pricing. The valuation from the latest funding round may not reflect the price at which a stake can actually be sold.

- Transfer restrictions. A company may have the right to approve a transaction or repurchase the shares first.

- Long holding periods. Buying shares on the secondary market does not guarantee that an IPO will happen soon.

- Concentration. The most accessible opportunities often involve companies that already carry the highest valuations.

- Transaction structure. An investor may be buying an interest in an SPV or another intermediary vehicle rather than owning shares directly, with separate fees and legal terms.

The entry price, legal structure, investor rights and realistic exit scenario therefore remain critical.

Will the secondary market solve the liquidity problem? Not entirely, at least not yet. The market has already exceeded $100 billion, while major financial institutions are actively expanding infrastructure for private transactions. This suggests a structural shift rather than a temporary trend. Secondaries are likely to become a permanent feature of the venture capital industry.

However, the current market remains too concentrated and opaque to unlock the full $3.2 trillion in unrealized value. For thousands of less established companies, buyers remain scarce and fair pricing is difficult to determine.

The most likely outcome is therefore a mixed model. Secondary markets will provide partial liquidity before IPOs, major public listings will deliver full exits and acquisitions will remain the third major channel.

The bottom line

The venture capital market has reached historic scale, but its financial infrastructure has not kept pace with that growth. The industry has become highly effective at raising trillions of dollars and creating companies with enormous valuations, but less effective at converting those valuations into cash distributions for investors.

The $3.2 trillion in unrealized value reflects the scale of potential returns, but also the amount of capital that remains locked inside private companies.

The secondary market is becoming an important part of the solution. Its real test, however, is not whether it can facilitate transactions in the 20 most prominent startups, but whether it can extend liquidity to thousands of other companies.

For investors, the key question is no longer limited to how much a startup’s valuation may rise. It is equally important to understand who may eventually buy the stake, when that transaction could happen and at what price.

This material is provided for informational purposes only and does not constitute investment advice. Investments in private companies involve elevated risk, limited liquidity and the possibility of a total loss of capital.