Regolith ETFs After Three Months: Leaders, Laggards, and Gains of Up to +18.60%

In late January 2026, Regolith launched its ETF offering on the platform – 12 exchange-traded funds spanning the core sectors of the global market, from semiconductors and biotech to uranium and precious metals. Over the past three months, roughly 200 investors have allocated capital to these funds. Below we review the first months of performance: fund-by-fund dynamics and the macroeconomic backdrop driving the results.

ETFs as an Instrument and Their Role on Regolith

An ETF (Exchange-Traded Fund) is a listed fund that holds a basket of dozens or even hundreds of stocks. By buying a single ETF, an investor effectively takes a stake in an entire sector or index. It is far more convenient than building a portfolio by hand: there is no need to analyze each company individually, track earnings reports, or manually rebalance weights.

ETFs are one of the most widely adopted instruments in modern portfolios. Global ETF assets under management exceeded $14 trillion in 2024, and institutional investors rely on them to implement sector, regional, and thematic views.

The ETF offering on Regolith launched as a logical next step in the platform's product lineup. Regolith selected 12 ETFs from leading global asset managers – iShares, VanEck, Global X, ARK Invest, and SPDR – giving investors exposure to the most active themes of 2026 in a single trade: AI, nuclear energy, biotech, semiconductors, and the broad U.S. market.

Leaders: Semiconductors, Biotech, and Nuclear

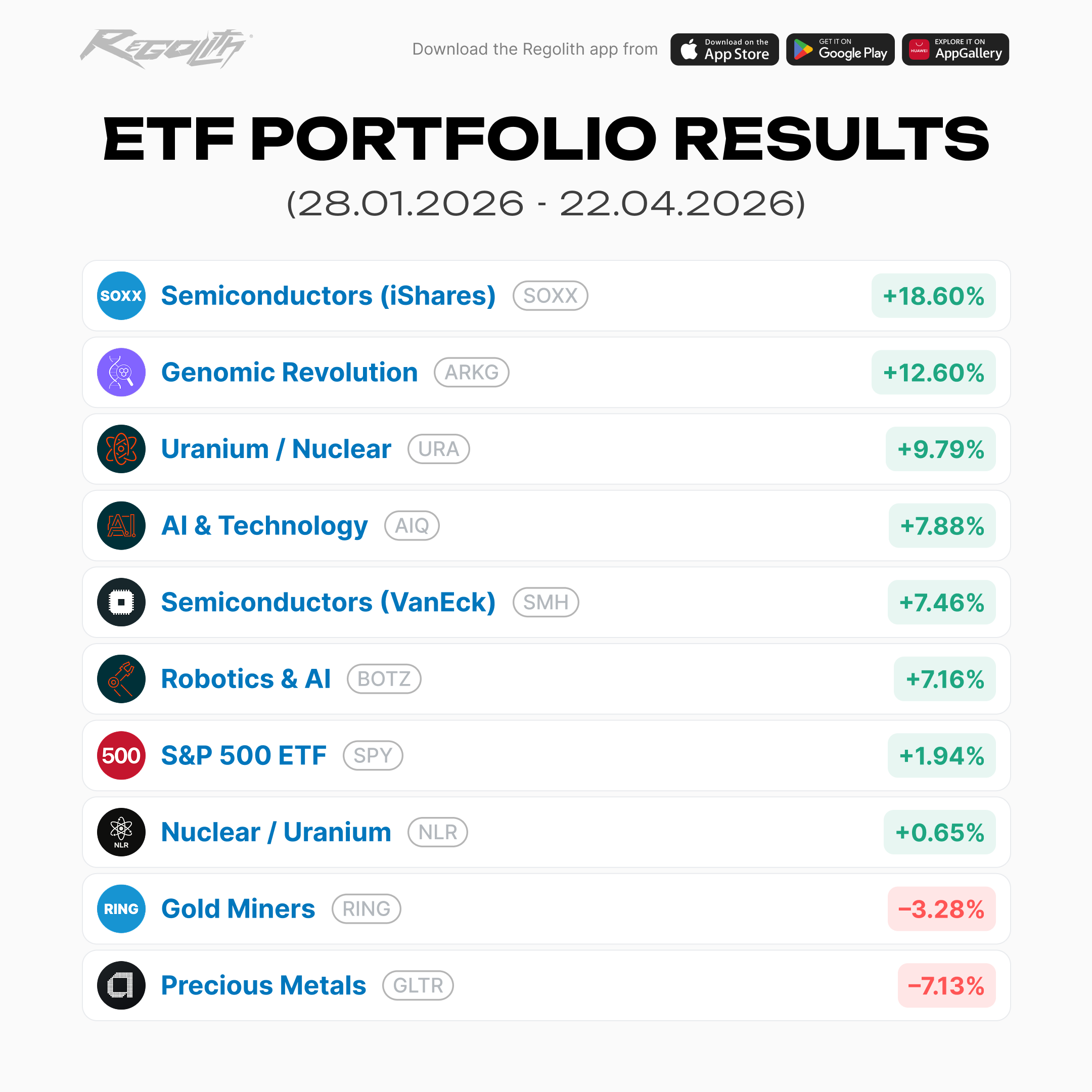

The top three performers are SOXX (+18.60%), ARKG (+12.60%), and URA (+9.79%). All three provide exposure to defining themes of the next cycle – AI chips, genetic medicine, and nuclear energy. Flows are concentrating here.

SOXX – iShares Semiconductor ETF (+18.60%)

SOXX leads the Regolith lineup. The basket holds the world's largest chipmakers – Nvidia, Broadcom, AMD, TSMC, Qualcomm, ASML, and Lam Research – the core suppliers of every modern data center and AI build-out.

- In April alone, SOXX gained 28.77% – the largest monthly move in the fund's 25-year history. Neither the dot-com rally of 2000 nor the crypto cycle of 2021 produced a print that large.

- Combined net inflows into SOXX and SMH hit $5.45 billion in a single month – an all-time high for the semiconductor category.

- AI chip revenue is projected to reach $500 billion in 2026, roughly half of total global semiconductor sales. That share stood below 10% as recently as 2022.

- Nvidia crossed $5 trillion in market capitalization in Q1 2026 – more than the combined value of the German stock market.

The driver is AI infrastructure spending. Microsoft, Meta, Google, Amazon, and Apple have guided combined capex above $400 billion in 2026 for data centers, GPU clusters, and training infrastructure. Each dollar of that spend flows through to the companies held in SOXX.

For investors, the takeaway is straightforward: even if the sector corrects in the short term, structural demand is set to extend for years.

ARKG – Genomic Revolution (+12.60%)

ARKG, ARK Invest's flagship biotech fund run by Cathie Wood, holds the companies reshaping frontier medicine: CRISPR Therapeutics, Intellia, Beam Therapeutics, Recursion, Twist Bioscience, and 10x Genomics.

The fund concentrates on three tracks:

- Gene editing (CRISPR and Prime Editing). The first FDA-approved therapies launched in 2023–2024, and second-generation precision-editing drugs are hitting the market in 2026.

- Personalized medicine. Treatments tailored to an individual's genome rather than applied uniformly across a patient population.

- AI-driven biology. Neural networks now identify drug candidates and predict protein structures orders of magnitude faster than classical methods. AlphaFold was only the opening act.

Biotech spent two years under pressure as high Fed rates pushed capital out of long-duration risk and into Treasuries. Rates began easing in 2026, and liquidity has returned to the sector. Successful clinical readouts on next-generation therapies have added conviction.

ARKG is one of the few single-ticker ways to gain exposure to frontier biotech without having to pick among dozens of still-unprofitable names.

URA – Uranium and Nuclear Energy (+9.79%)

URA is one of the standout funds of the 2025–2026 cycle. It pulled in $3.8 billion in inflows in 2025 and returned +156% for the year. The trend has continued into Q1 2026, though at a more measured pace.

The rally rests on a structural shift in global energy. AI data centers consume electricity on an industrial scale. The International Energy Agency projects that by 2030, data centers will account for 8–10% of global electricity consumption – up from 1–2% today.

- Renewables alone cannot deliver the baseload needed to keep AI hardware running 24/7, moving nuclear back into the planning mix.

- In 2025, the U.S. passed its largest package of nuclear support in four decades – production tax credits, fuel-supply guarantees, and accelerated licensing for new reactors.

- China and India continue to expand capacity, Japan has restarted previously idled reactors, and Europe has softened its anti-nuclear stance.

The market's focus is on small modular reactors (SMRs) – compact plants that can be built in three to four years versus ten to fifteen for conventional stations. Leading names include Oklo, TerraPower (backed by Bill Gates), NuScale, and X-energy. The first U.S. SMRs are targeted for commissioning in 2027–2028.

URA gives exposure to the uranium miners (Cameco, Kazatomprom, NexGen Energy, Uranium Energy Corp) and to the service companies supporting the new nuclear fuel cycle. Spot uranium has moved from $40 to $95 per pound over the past two years, and long-term contracts between producers and utilities are pricing in $120–140 by 2028.

AIQ, SMH, and BOTZ: Three Different Angles on AI

Three more funds are firmly in positive territory – AIQ (+7.88%), SMH (+7.46%), and BOTZ (+7.16%). Each plays the AI theme differently.

AIQ – Global X AI & Technology (+7.88%)

AIQ is the broadest AI fund in the selection. Its basket moves beyond pure chipmakers to include software developers, cloud providers, cybersecurity firms, and data infrastructure companies.

Top holdings: Nvidia, Microsoft, Meta, Alphabet, Oracle, Palantir, ServiceNow, CrowdStrike, Palo Alto Networks, Snowflake. AIQ is effectively a cross-section of the full AI stack – from silicon and cloud infrastructure to applications and security.

Why the mix matters:

- AI revenue runs across the full value chain. Nvidia monetizes GPUs, Microsoft and Oracle monetize compute, Palantir and Snowflake monetize data, and CrowdStrike and Palo Alto monetize the security layer around AI systems.

- Concentration risk is lower than in SOXX. A correction confined to semiconductors is partly offset by the fund's software holdings.

- AIQ serves as a broad AI vehicle for investors who want thematic exposure without the volatility of pure chipmakers.

Since the start of 2024, AIQ's AUM has grown roughly 3.5x, placing it among the primary beneficiaries of capital rotating into AI.

SMH – VanEck Semiconductor ETF (+7.46%)

SMH is the main competitor to SOXX – a semiconductor fund built on a different weighting logic.

- Top-heavy construction. SMH's top ten holdings account for roughly 70% of assets, and TSMC and Nvidia alone make up close to 30%. Moves are sharper in both directions: faster on positive catalysts, deeper on leader-driven drawdowns.

- SOXX is more evenly distributed, with single-name weights capped near 8–9%. Lower volatility, lower upside peaks.

- SMH carries heavier Asian exposure – TSMC, ASML (via ADR), and Tokyo Electron – making it more sensitive to Taiwan geopolitics and U.S.–China trade policy.

Over the past five years, SMH has outperformed SOXX on a total-return basis, largely on the back of its TSMC weighting.

Both funds are in the selection because they offer distinct ways to play the same sector – SOXX for more even diversification within the theme, SMH for concentrated exposure to the top names.

BOTZ – Robotics & AI (+7.16%)

BOTZ is the most "physical" AI fund in the group. Its focus is automation, robotics, and industrial AI – companies translating software breakthroughs into hardware, robots, and autonomous systems.

Top holdings:

- Intuitive Surgical – maker of the da Vinci surgical robots.

- ABB – Swiss industrial leader in factory robotics.

- Fanuc – Japanese manufacturer of industrial robots.

- Keyence – sensors and measurement systems for automated production.

- Nvidia – here in its role as the chip supplier for autonomous systems.

- Dynatrace, UiPath – enterprise automation through AI.

BOTZ is a direct play on embodied AI: robots, drones, medical devices, and autonomous vehicles – the stage of AI that follows large language models, where neural networks begin acting on the physical world.

Key 2026 catalysts:

- Humanoid robotics. The first production humanoids from Tesla (Optimus), Figure AI, 1X, and Agility Robotics are reaching enterprise customers. BCG projects the humanoid market at $100 billion by 2030.

- Logistics automation. Amazon, DHL, and Walmart are accelerating warehouse robotization, supporting demand for names held in BOTZ.

- Surgery and medtech. Intuitive Surgical posted record da Vinci shipments in 2025.

The stronger embodied AI becomes, the more the fund tracks upward. BOTZ is a bet that the coming decade will be defined as much by robotics as by software.

SPY and NLR: Slower-Moving Positions

SPY (+1.94%), the largest ETF tracking the S&P 500, functions as a proxy for the U.S. market. The modest return reflects March's correction, which erased a large portion of the January–February gains. The recovery is ongoing but uneven: the top six or seven tech names are pulling the index higher, while the rest of the market lags.

NLR (+0.65%) is the second nuclear ETF in the selection, but with a more defensive structure. Alongside uranium miners, it holds major utility operators – Duke Energy, Constellation Energy, and Dominion. These names pay dividends and carry lower volatility, but also trail during periods of rapid sector expansion. NLR offers a more conservative way to access the nuclear theme.

Laggards: Gold and Precious Metals

RING (–3.28%), the Gold Miners ETF, shows the paradox of the current market: the gold price remains elevated, yet miners are trailing. Several drivers are in play:

- Higher mining costs – electricity, fuel, and wages.

- Regulatory constraints in a number of jurisdictions.

- Inflation pressure on operating expenses.

Historically, this is a familiar pattern – miners do not always move in step with the underlying metal. For patient capital, such windows can create opportunities: once operating costs stabilize while metal prices hold up, miner margins tend to rebound quickly.

GLTR (–7.13%) is a basket of four precious metals: gold, silver, platinum, and palladium. The drag comes primarily from platinum and palladium – metals traditionally used in automotive catalytic converters, where demand is falling as the EV mix expands.

What the Numbers Say About the Market

The fund results are a clean read on where capital is moving.

Main drivers of 2026

- AI infrastructure: chips, networks, data centers, cloud capacity

- Nuclear energy: reactors back on the agenda as electricity demand rises

- Biotech and genomics: capital returning after two years of pressure

Sectors under pressure

- Precious metals: falling auto-industry demand for platinum group metals

- Mining: rising costs and regulatory headwinds

Neutral zone

- Broad U.S. market: positive but without strong momentum – concentrated in a handful of tech leaders

For investors, the signal is clear: capital is rotating toward sectors with structural multi-year demand, while short cyclical rebounds take a back seat.

12 Funds, 12 Different Logics

The 12 ETFs differ in risk and return profile – a direct function of the sectors they cover and how each portfolio is built.

- Concentrated sector funds with capital focused on the leaders – SOXX, SMH, ARKG, URA. These hold names from fast-growing industries (AI, semiconductors, biotech, uranium). Historically, such funds show large moves in both directions: strong gains during sector booms, deeper drawdowns when the cycle turns.

- Broad thematic funds – AIQ, BOTZ, NLR. These span several segments within a theme. AIQ combines chipmakers with software, cloud, and cybersecurity, while NLR pairs uranium miners with major utility operators. The wider basket softens the impact of single-company drawdowns.

- Broad-market index funds – SPY. Tracks the 500 largest U.S. public companies and reflects the overall economy. Lower volatility than sector plays, and typically moves in line with the broader market.

- Precious metals and mining funds – GLTR, RING. These follow the logic of commodity cycles, driven by metal prices, production costs, and industrial demand. Correlation with technology is low, so their behavior often runs counter to the rest of the basket.

Understanding these distinctions helps form a clearer picture of how each fund can behave across different market conditions.

What's Ahead: Online Trading and New Funds

Regolith is preparing to roll out online ETF trading in the near term – buying and selling directly from the app, without manual requests or waiting periods. Execution will be in a single click, as on a conventional brokerage account.

In parallel, the team is expanding the selection. Funds covering defense, emerging markets, renewable energy, and thematic strategies are in preparation.

Risks

ETFs are a convenient instrument, but not a guarantee of returns. Key points:

- Past performance is not indicative of future results.

- Sector ETFs (AI, uranium, biotech) are sensitive to market sentiment and can correct sharply.

- All funds are USD-denominated – currency risk applies to investors in local currencies.

- ETF investments are not insured and can lose value.

Any allocation should be made with reference to an investor's financial situation and investment horizon.

Conclusion

The first three months of ETFs on Regolith have coincided with a period of global market repositioning. Capital is rotating aggressively into semiconductors, biotech, and nuclear energy. Each of these themes represents a multi-year structural trend reshaping global investment flows.

All 12 funds are already available in the Regolith app. If you would like to see a specific sector or fund added to the selection, let us know – the platform incorporates client input when expanding its product offering.